Section 180:

Restriction on Power of Board

·

*

According to section 180(1), Board need the prior approval of shareholders by passing

the SR at GM for exercising the following powers:

a.

Sell,

lease or otherwise dispose of the whole, or substantially the whole of

undertakings of the company.

b.

Invest,

otherwise than in trust securities, the compensation received in respect of

the compulsory acquisition of any undertaking of the company as a result of

merger or amalgamation.

c.

Borrow

moneys, if money already borrowed, together with moneys to be borrowed will

exceed the aggregate of paid up capital

and free reserves of the company.

d.

Remit, or

give time for the repayment of any debt due by a director. However, advance

given in the ordinary course of business to a director may be renewed by a banking company without the approval of

the GM.

·

*

Section 180 applies to all companies.

Undertaking

It means undertaking in which company has

made investment more than 20% of its net worth or undertaking which generates

20% of the total income as per the last audited balance sheet.

Net

worth

Aggregate value of paid up capital (+) all

reserves created out of profits and securities premium amount (-) accumulated

losses, deferred expenditure and miscellaneous expenditure not written off as

per last audited balance sheet.

Substantially

the whole of undertaking

It means in any financial year, 20% or more

value of undertaking as per last audited balance sheet.

Section 181: Donation

to charitable funds

·

* BOD of company may contribute or donate to bona fide charitable and other funds with

prior approval of GM when such aggregate

amount of contribution in any financial year, exceeds 5% of its average net profit for 3 immediately preceding

financial year.

·

* Any amount spent for welfare of employees is

within the scope of charitable contribution.

·

* The resolution

passed by the shareholders in GM must

specify the total amount upto which moneys may be contributed by Board.

·

* Section 181 is applicable to all companies.

Section 182:

Political Contributions

·

*

Contribution means any payment made without consideration. It includes donation, subscription or any

other payment. It includes contribution made to:

-> Political party

-> Person for political purpose.

·

* Section 182 covers

political contribution made whether directly or indirectly. Directly means

company has contributed towards any expenses for political party or donation

made to political party. Indirect contribution means payment made to any person

for benefit which political party has obtained from that person.

Example:

Expenditure incurred by company on printing and distribution of posters and

leaflets for political party.

·

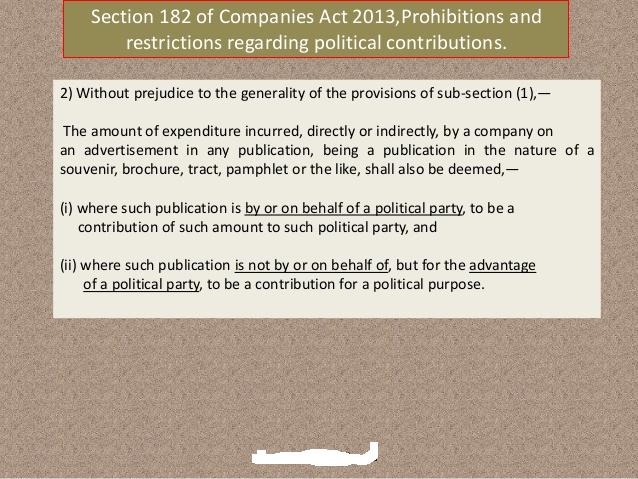

*

It also includes any expenditure incurred by a

company on advertisement in any

publication by or on behalf of a political party or for its advantage.

Point

to be noted

Any assistance, donation and contribution

to a political party or for political purpose, made through means other than

money, but which is quantifiable and capable of being expressed in monetary

terms is also covered under section 182.

·

* Government

companies and companies which

have been in existence for less than 3 financial years are not allowed to make political contributions.

Political contribution may be made by

any other company subject to the following conditions:

-> The aggregate amounts contributed and proposed

to be contributed by a company in any financial year shall not exceed 7.5% of its average net profits of preceding last 3

financial years.

-> Board

resolution should be passed.

·

* Disclosure

in P & L A/C

-> The amount

of contributions during the financial year.

-> The name

of the party or person to which amount has been contributed.

Penalty for contravening the

provisions of section 182

-> Company –

Maximum fine: 5 times the amount so contributed

->Officer

in default – Maximum imprisonment: 6 months, Maximum fine: 5 times the amount so

contributed.

Section 183: Contribution to

National Defence Fund

·

*

Company can contribute any amount to national defence fund or any other fund approved by

CG for the purpose of defence fund.

·

* Amount can be contributed to national defence

fund by board of directors or any person

or authority exercising powers of board or of the company in general meeting.

·

* Section

183 overrides section 180, 181, 182 and anything contained in MOA or AOA of

company.

·

*

Company should disclose the total amount contributed to national defence fund in its P & L A/C during the

financial year.

No comments:

Post a Comment